Managing Consignment Goods in MRPeasy

Consignment inventory is an inventory management and purchasing method wherein the goods procured from a vendor remain in the ownership of the supplier until they are sold or consumed. Here is how our US-authorized consultants Business Solution Providers, Inc. implemented consignment inventory for a client.

About the Author: Denis Baldwin (denis@businesssp.com) is an MRPeasy Implementation Engineer with Business Solution Providers, Inc. (www.businesssp.com). For more creative solutions to your MRPeasy challenges, the team at BSP is here to help you!

Consignment inventory and the business case

A client of ours, Kerfkore (www.kerfkore.com), a manufacturer of architectural panels and other wood-formed goods, needed to manage consignment goods in their operation. While most of the items purchased by the client for manufacturing were purchased in traditional terms from vendors, one vendor offered open-ended consignment terms, allowing the client to pay for these goods as they were consumed, not as they were purchased. The benefits to cash flow were obvious to the client, but they were concerned about how holding this inventory, often in the tens of thousands of dollars, would throw their balance sheets into disarray. What would appear to be an asset as raw goods would actually be considered a liability (as the vendor still owns the consigned goods being stored in the client warehouses, and the client still owes the vendor for these goods). To complicate things further, these raw goods are sometimes purchased from other vendors, or from this vendor as cash upon receipt, so there needed to be a clear line between the various impacts these items could take financially.

Consignment represents a unique problem for both accounting and inventory management, as the goods are not technically “owned” by the client, even though they are holding the inventory. This represents challenges both in inventory valuation and skews that inventory in terms of both potentially being an asset and a liability. Per the terms between the client and their vendor, these would be payable at the time of consumption. These are fairly fast-moving raw goods but the hold time between receipt and manufacture could vary wildly from a few days to a few months, depending on the volume of consignment stock received, and product demand – both in terms of manufacturing capacity (for build to stock) and customer demand.

With the standard method of purchasing and accounting for goods in MRPeasy, the client would send out a purchase order for the expected cost of goods to the vendor, receive these items into inventory at the price paid, and carry the financial burden of these goods throughout their process. Because of this, goods that were not paid for would appear to affect both the value of goods on hand and the financial impact of paying for these goods.

MRPeasy has no process for consignment built into the system yet, and this workaround is a bit cumbersome, but it does appear to accomplish the goal of separating financial impact from physical inventory.

Some caveats to consider

- You can not have more than one item from the same consignment issuing vendor on a PO, or else the billing part will not work. i.e. you would not be able to receive several items in full quantity and then later invoice off just part of one item. All part numbers need to receive at least some quantity of each line item on the PO consumed at once or none. For this reason, we recommend one line item per purchase order for this process.

- Depending on your vendor, you may need to realize financial impact at different times, either at manufacture, at 30 days, at the end of a quarter, all at once (i.e. must consume all they sent at once interval, even if it’s months later). These terms are different from vendor to vendor.

- If you do not change the item cost before manufacturing, it will skew your production costs lower than they actually are.

- YMMV, depending on how you do your accounting. We advise doing testing and auditing both MRPeasy and your accounting system between each step to see the financial impact and how it is recorded.

A few settings to check and configure

For the purpose of separating this consigned inventory from the operational inventory, a second site was established as a “virtual hold location” for these items. This location was used to receive the goods, specified as such on the purchase order. To accomplish this in MRPeasy, we needed to make a few changes in the software’s System Settings:

- System Settings > Usability Settings > Multiple Stocks and Production Sites (set to yes).

- System Settings > Software Settings > Several Invoices Per PO (set to yes).

- System Settings > Software Settings > “separate invoices and deliveries” (set to yes).

Physically and technically separating the inventory flow

How you sort and account for the management of your physical consigned goods in comparison to your self-owned inventory will depend on your space constraints and other factors, but it is important to note that these stock locations can be financially and logically/systematically different but physically together, if necessary. With diligent lot tagging and carefully managing your stock lots, a physically constrained common area could work, but it is not advised.

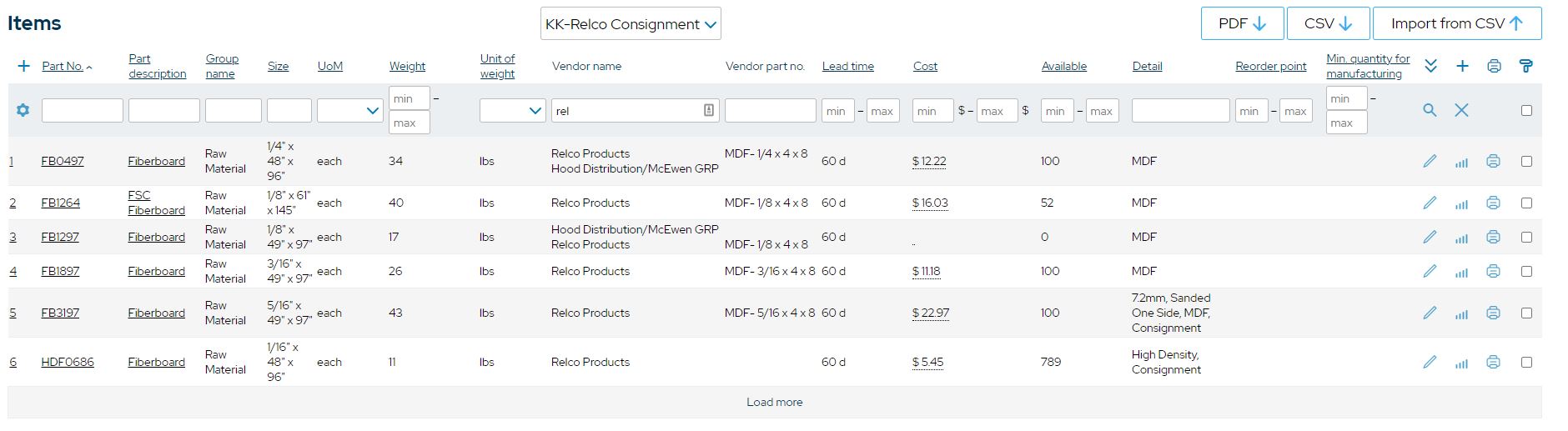

This does not mean you have to have a separate building, but having a separation of any kind two buildings, two rooms, two pallet spaces, and different color tape on the floor that signifies “this is consignment” will go a long way in making this more manageable. Since only one vendor has consignment terms with this client, this made segregating these items easy by filtering only those vendor’s items in the STOCK > ITEMS view by the vendor:

The linked MRP document trail acts as your chain of custody

When requesting the goods from the vendor, the client sent out a purchase order to the vendor for the items, including the actual costs they would pay for the items after those items were consumed. The consignment virtual location was used as the receiving point on the purchase order. This PO was saved and sent to the vendor and downloaded as an “internal PDF” before saving. These Purchase Order hard copies are set aside by the purchasing agent and stamped “consigned, not paid” so they could be processed further when the materials are consumed in manufacturing. If you want to double down on accountability, consider adding a custom field to the Purchase Order template of “consignment order (yes checkbox)” so these could be filtered inline in the purchase orders view.

Once the vendor acknowledged the purchase order, the purchasing agent edited the PO to bring the costs to $0.00 for the items purchased and saved the purchase order. The purchase order will remain this way, with zero cost for the goods ordered, until manufacturing is ready to begin.

Lot management helps… a lot

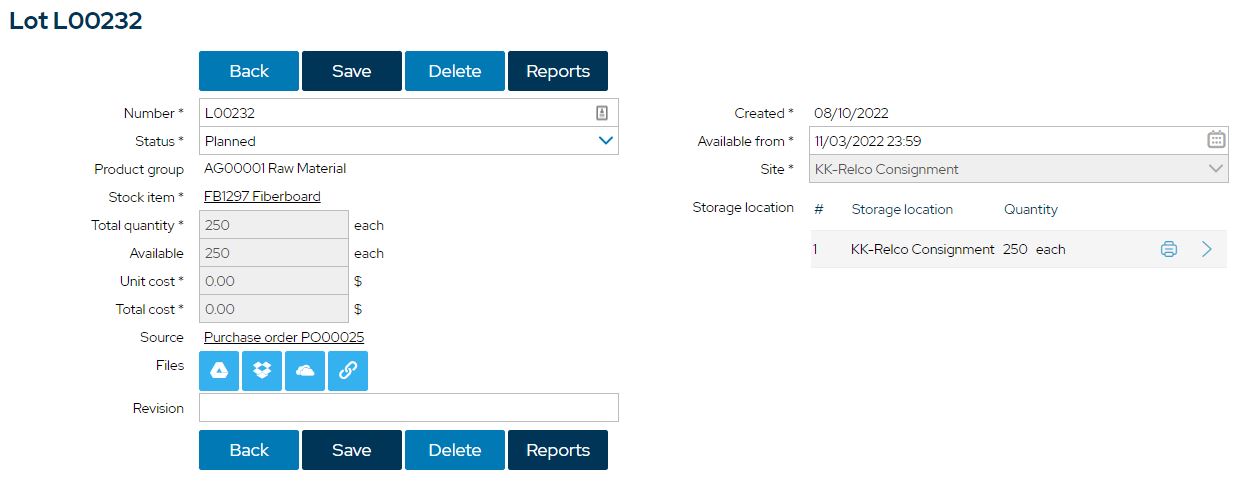

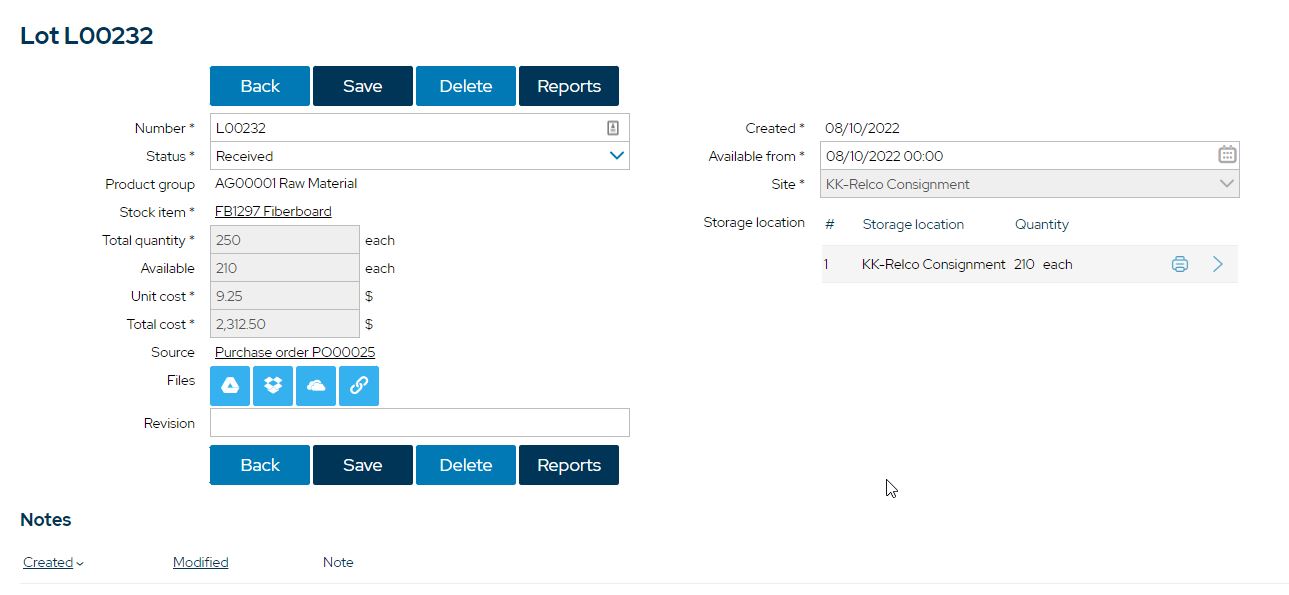

When the PO was saved, a lot was created (Lot L00232). This lot now showed the cost of the goods at $0.00 and stored in the consignment location. We use this lot tracking as a reference throughout this process as it shows us the cost associated at each step.

When the order is received from the vendor, it is stored with the lot number on the printed label and placed in the “hold-consignment” part of the warehouse, a “virtual site” within MRPeasy. In addition to the lot detail, we can also see in the stock history the assumed cost of the goods at this step and at each movement throughout the system.

Receiving your PO, in full, to your new stock site

When the consignment order comes in, receive your goods as you would with any purchase order/delivery receipt. Your receiving staff should confirm that the location (consignment site) on the Purchase Order matches the designated storage location for the consigned goods and a stock lot sticker is printed and affixed to the lot. Regardless of how many you will be using for production (and thus costing at that time), receive the entire lot to the consignment site at this time.

A customer placed an order for the finished good “FK200FB12” later that day, which uses the two pieces of the “FB1297” consignment part to produce one finished good. As there is none of the raw material available in stock in the main storage area, 40 pieces will need to be transferred from consignment stock.

Transfer Orders: releasing your consigned goods to be consumed

At this time, a transfer order is created from the virtual consignment site to their manufacturing site. In the interest of only absorbing the costs for the amount of material to be consumed today (and thus invoiced to the vendor today) a transfer order of 40 units is made.

Creating this transfer order does a few things from a transaction logging perspective:

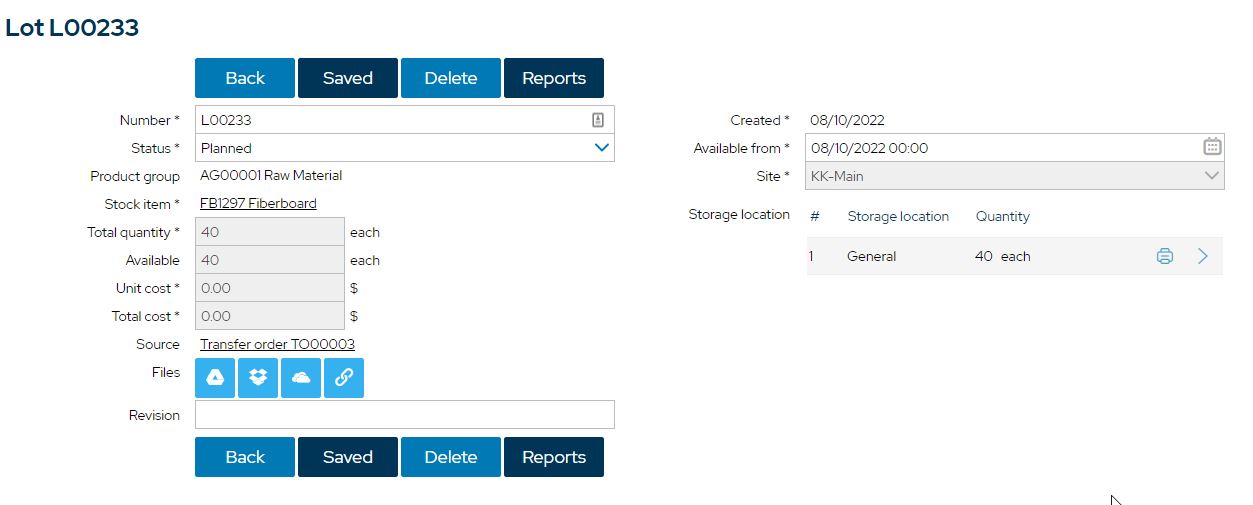

- Setting “from” to the consignment location and “to” to the main storage area will create a Booking, a new lot, and a transfer order – 3 stops in stock history that can be tracked, with the current cost of $0.00 for the items.

- The status of the transfer order will, after picking, be set to “shipped.” When these consigned goods are received in common stock, a designated person will set the status to “received”, indicating that the chain of custody has moved forward.

- The previous lot (LO0232) still exists after the transfer, now 40 units less (250 originally allocated to consignment stock, now 210 remain). This can be verified by looking at the Lot detail:

This action created a new lot number for the 40 units moved to the main stock, Lot L00233. The items were picked, both in the transfer order and physically in the warehouse, and moved to production staging. As you can see, at this point, the realized cost of the materials is still $0.00.

Invoicing and updating the PO, realizing costs the moment before manufacturing

After the transfer is complete, but before manufacturing orders are started, the purchasing department will make three financial-impacting steps to realize the true cost into operations:

- Update Previous Purchase Order – open the purchase order that previously had the costs at zero for the consignment items (PO00025) and update the cost at the line item for the consigned goods, now ready for consumption.

- Create the Invoice – In the Purchase Order Record, create an associated invoice for 40 of the units. This invoice will be made out for the actual price ($9.25 per unit) from the vendor. If there is no vendor invoice number known, I recommend putting the PO number and today’s date as the invoice number (i.e.. PO00025-2022-08-10), as there will be more invoices tied to this purchase order in the future, as more of the consignment stock is consumed.

- Make an associated payment – As the payment terms of the consignment agreement state that goods will be paid-for upon consumption, log a payment for the materials to be used. If there is variance/potential waste in production for this raw material, you may want to save these documents but not cut checks or otherwise close these out until after manufacturing is finished for this lot of consigned materials.

Manufacturing Order commitment incorporates the actual cost

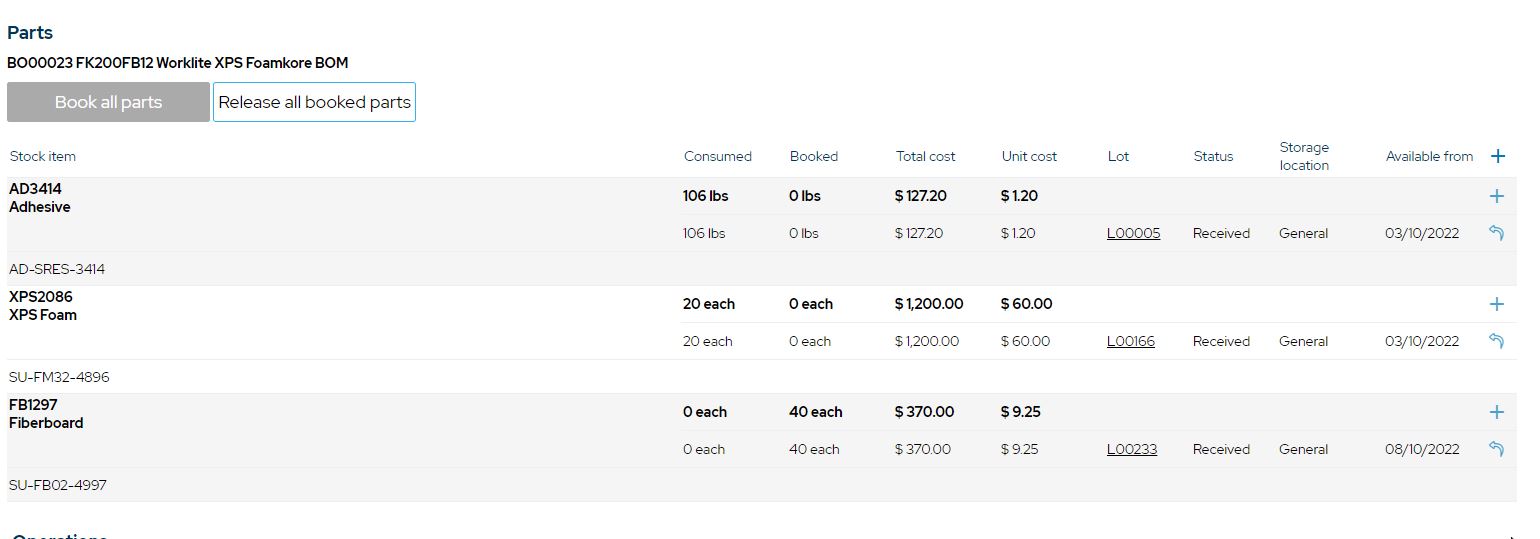

As the above purchasing tasks affected the financials but not the inventory physically, you will see no change in stock history to signify the costs being realized until manufacturing is completed. As the client had a need to produce 20 units of finished goods FK200FB12 (which contains our previously consigned FB1297), a manufacturing order is processed (MO00014) using 40 total units of FB1297 to produce 20 units of finished goods FK200FB12.

The first indication is that the cost of the consigned items is now reflecting the actual cost. Look at the details in the bill of material. The line item for FB1297 will reflect the actual cost:

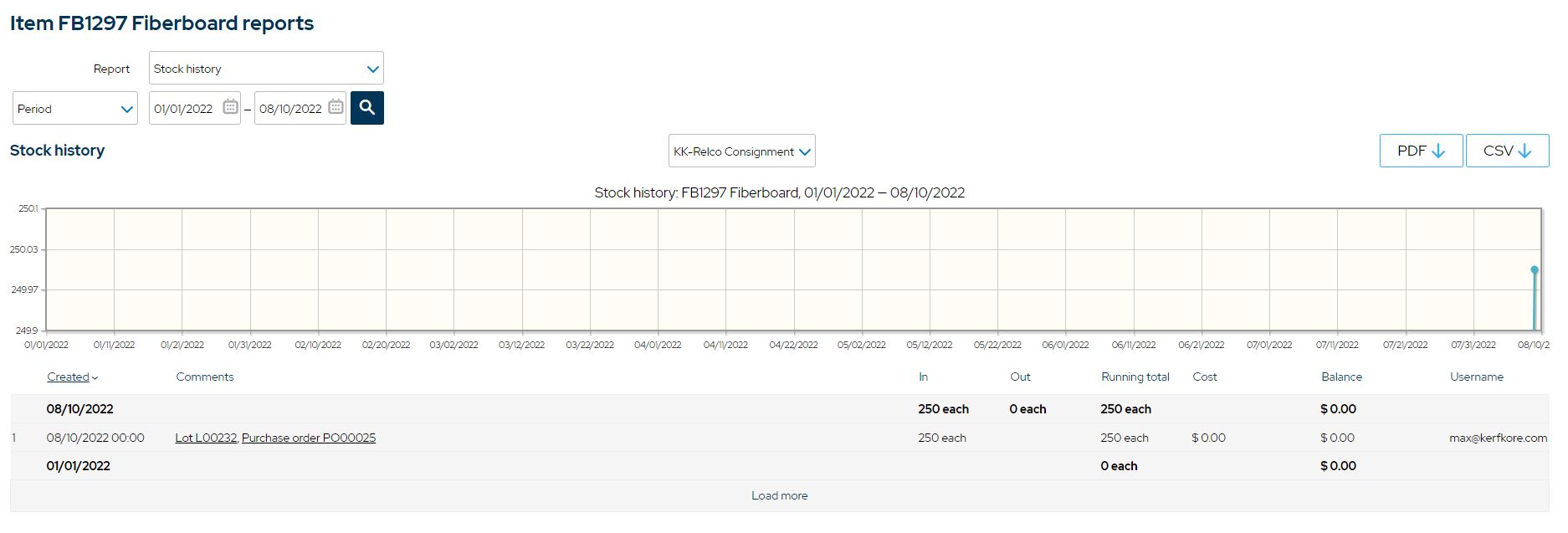

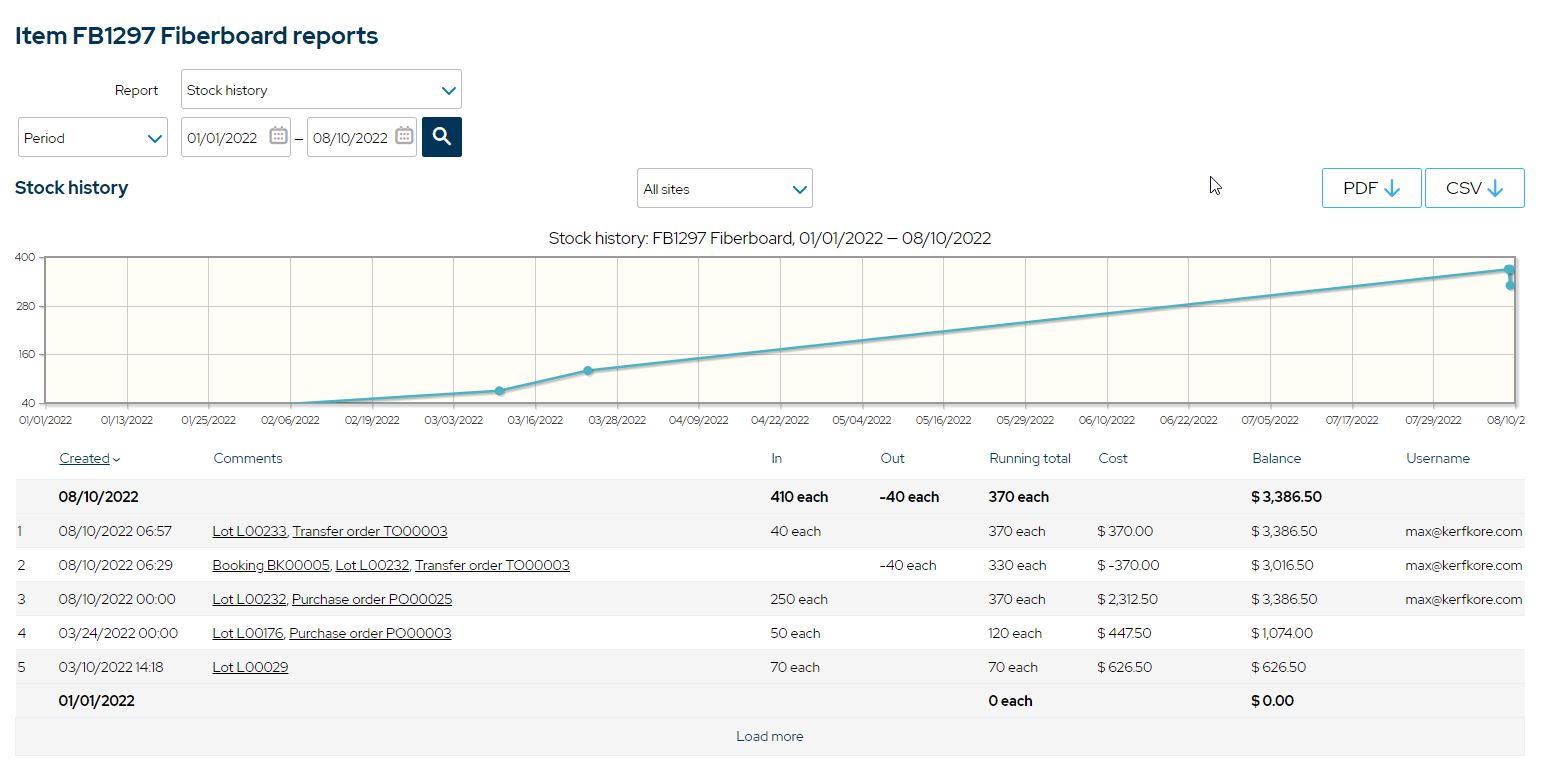

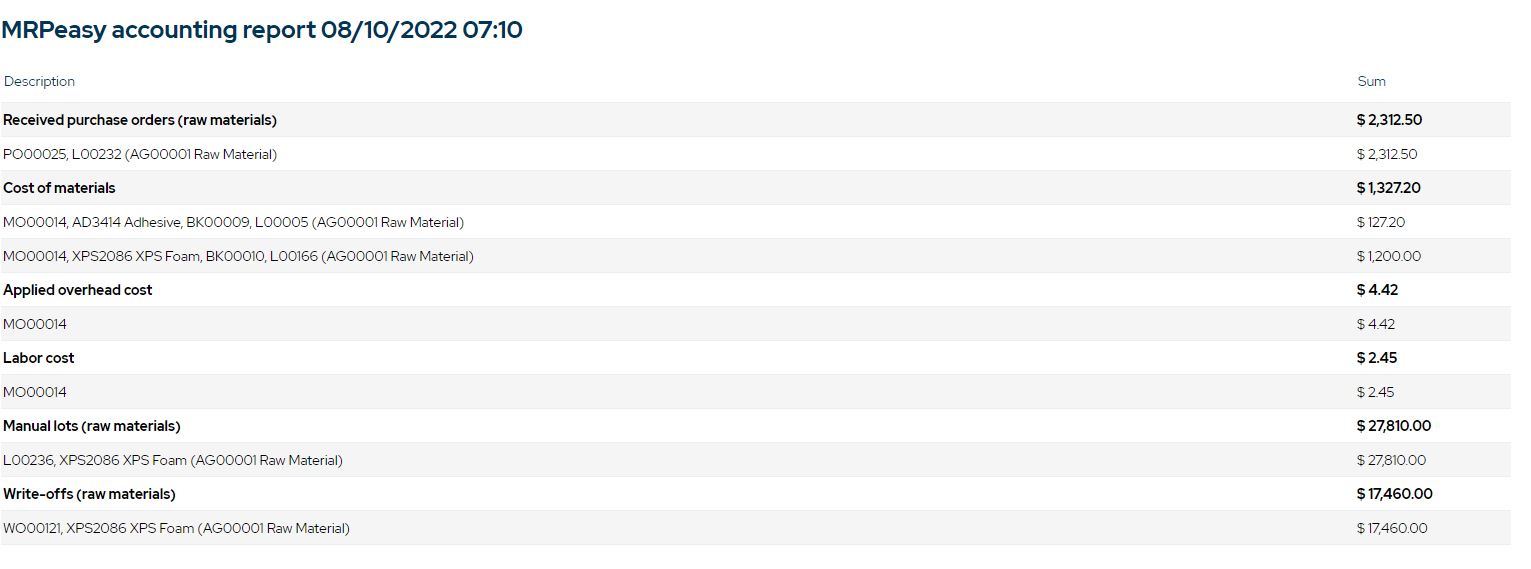

Review the Item Reports/Stock History to see the chain of custody and costs applied

Final confirmation, audit the process in your accounting system

To confirm that all costing was applied properly throughout the process, a review of the lots at each step and a stock report on the raw item was reviewed above. If you are using Quickbooks Online, the transactions can be seen at each step as well in the synchronization log between MRPeasy and QBO. Review that the proper accounts are being updated by this process in your accounting system.

Before you “consign yourself” to not tracking your consigned goods properly in MRPeasy, give this workaround a try. If you need help, consider reaching out for a free review of your needs. Hourly and full project MRPeasy Implementation support, training, integrations, and more are available from the team at Business Solution Providers.